Three Types of Pensions

When planning for retirement, one critical aspect to consider is your pension. Pensions provide a reliable source of income during retirement, ensuring financial stability and peace of mind after leaving the workforce. There are three main types of pensions available, each with its unique features and benefits. In this article, we’ll explore these three main types: defined benefit pensions, defined contribution pensions, and state pensions. This latest news aims to give you a clear understanding of these pension systems and how they can impact your retirement planning.

Types of Pensions Explained

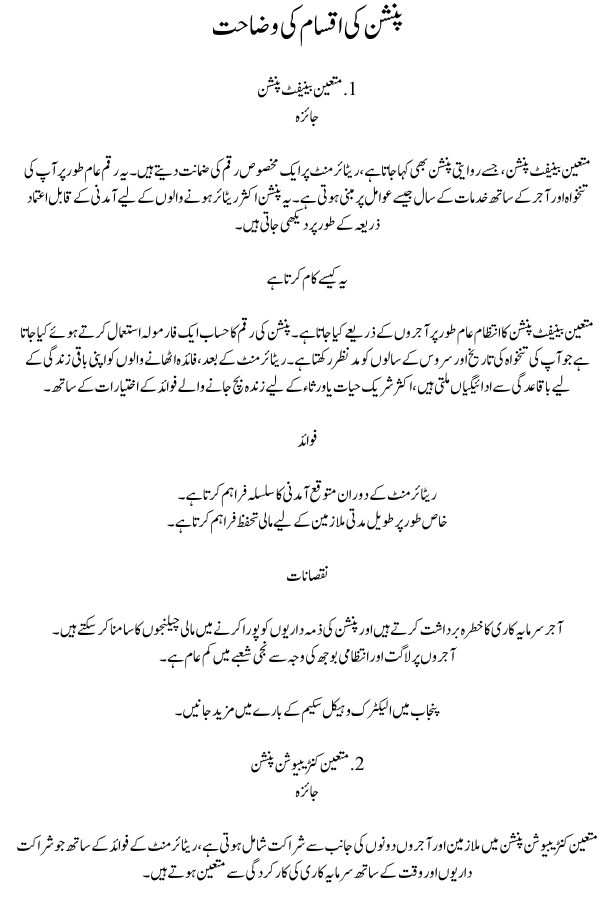

1. Defined Benefit Pensions

Overview

Defined benefit pensions, also known as traditional pensions, guarantee a specific amount of income upon retirement. This amount is usually based on factors like your salary and years of service with an employer. These pensions are often seen as a reliable source of income for retirees.

How It Works

Defined benefit pensions are typically managed by employers. The pension amount is calculated using a formula that takes into account your salary history and years of service. Upon retirement, beneficiaries receive regular payments for the rest of their lives, often with options for survivor benefits for spouses or heirs.

Advantages

- Provides a predictable income stream during retirement.

- Offers financial security, especially for long-term employees.

Disadvantages

- Employers bear the investment risk and may face financial challenges in meeting pension obligations.

- Less common in the private sector due to cost and administrative burdens on employers.

Learn more about the Electric Vehicles Scheme in Punjab.

2. Defined Contribution Pensions

Overview

Defined contribution pensions involve contributions from both employees and employers, with retirement benefits determined by the contributions made and the performance of investments over time.

How It Works

Contributions are regularly made into individual retirement accounts, similar to 401(k) plans in the United States. Employees often have control over investment options within the plan. The retirement benefit depends on factors like contribution amounts, investment returns, and the length of time invested.

Advantages

- Offers flexibility and portability, allowing individuals to take their retirement savings with them if they change jobs.

- Provides potential investment growth over time.

Disadvantages

- Retirement income isn’t guaranteed and can vary based on investment performance.

- Requires individuals to take an active role in managing their investments, which can be challenging for some.

Read more about the new pension system in Pakistan.

3. State Pensions

Overview

State pensions, also known as social security or public pensions, are government-administered programs designed to provide income during retirement. They are often seen as a safety net for retirees.

How It Works

Eligibility and benefit amounts vary by country and are often based on factors like age, income, and years of contributions. Funding typically comes from payroll taxes or other government revenue sources. Benefits may be adjusted periodically based on factors like inflation or changes in population demographics.

Advantages

- Provides a safety net for retirees, especially those without other sources of retirement income.

- Offers a source of income that is adjusted for inflation, providing some protection against rising living costs.

Disadvantages

- Benefits may not be sufficient to cover all retirement expenses, especially in regions with high living costs.

- Sustainability concerns exist in some countries due to growing populations and strains on government budgets.

For more details, check out Applying Online for NAVTTC Batch 4.

Comparing the Three Types of Pensions

| Feature | Defined Benefit Pension | Defined Contribution Pension | State Pension |

|---|---|---|---|

| Retirement Benefit | Guaranteed income based on salary and years of service | Depends on contributions and investment performance | Government-administered benefit based on eligibility criteria |

| Investment Risk | Employer bears investment risk | Individual bears investment risk | Government-backed, but subject to economic and demographic factors |

| Portability | Generally not portable | Portable, can be transferred between jobs | Typically tied to residency or citizenship |

| Control over Investments | Limited, managed by employer or pension fund | High, individuals select investment options | N/A, managed by government |

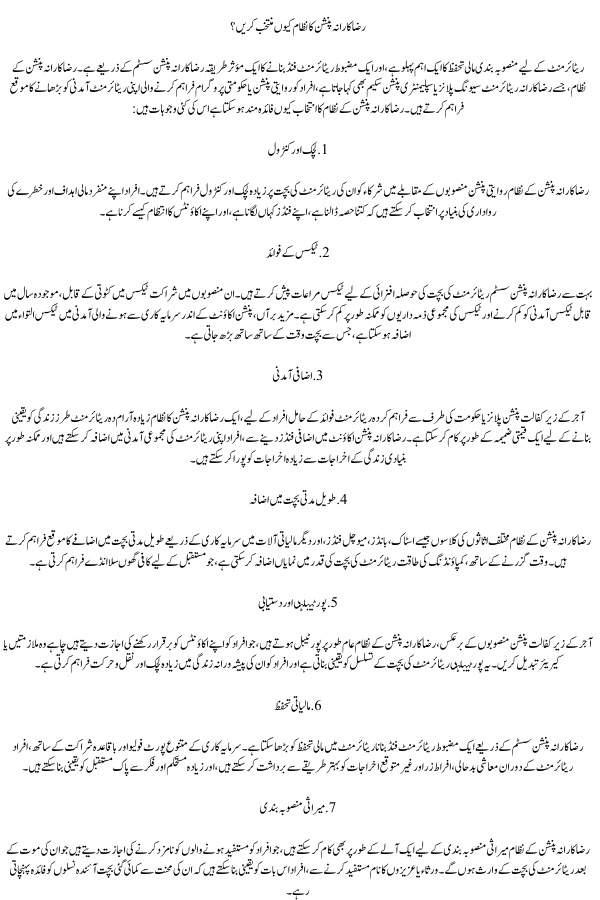

Why Choose a Voluntary Pension System?

Planning for retirement is a crucial aspect of financial security, and one effective way to build a robust retirement fund is through a voluntary pension system. Voluntary pension systems, also known as voluntary retirement savings plans or supplementary pension schemes, offer individuals the opportunity to supplement their retirement income beyond what traditional pensions or government programs provide. Here are several reasons why choosing a voluntary pension system can be beneficial:

1. Flexibility and Control

Voluntary pension systems offer participants greater flexibility and control over their retirement savings compared to traditional pension plans. Individuals can choose how much to contribute, where to invest their funds, and how to manage their accounts based on their unique financial goals and risk tolerance.

2. Tax Benefits

Many voluntary pension systems offer tax incentives to encourage retirement savings. Contributions to these plans may be tax-deductible, reducing taxable income in the current year and potentially lowering overall tax liabilities. Additionally, investment earnings within the pension account may grow tax-deferred, allowing savings to compound over time.

3. Supplemental Income

For individuals with employer-sponsored pension plans or government-provided retirement benefits, a voluntary pension system can serve as a valuable supplement to ensure a more comfortable retirement lifestyle. By contributing extra funds to a voluntary pension account, individuals can increase their overall retirement income and potentially cover expenses beyond basic living costs.

4. Long-Term Savings Growth

Voluntary pension systems offer the opportunity for long-term savings growth through investments in various asset classes such as stocks, bonds, mutual funds, and other financial instruments. Over time, the power of compounding can significantly increase the value of retirement savings, providing a substantial nest egg for the future.

5. Portability and Availability

Unlike employer-sponsored pension plans, voluntary pension systems are generally portable, allowing individuals to maintain their accounts even if they change jobs or careers. This portability ensures continuity of retirement savings and provides individuals with greater flexibility and mobility in their professional lives.

6. Financial Security

Building a robust retirement fund through a voluntary pension system can enhance financial security in retirement. With a diversified portfolio of investments and regular contributions, individuals can better withstand economic downturns, inflation, and unexpected expenses during retirement, ensuring a more stable and worry-free future.

7. Legacy Planning

Voluntary pension systems can also serve as a tool for legacy planning, allowing individuals to designate beneficiaries who will inherit their retirement savings upon their death. By naming heirs or loved ones as beneficiaries, individuals can ensure that their hard-earned savings continue to benefit future generations.

Final Thoughts

Choosing the right pension plan is a crucial decision that can significantly impact your financial well-being in retirement. Understanding the differences between defined benefit, defined contribution, and state pensions is essential for making informed choices about retirement planning. While each type of pension has its own advantages and disadvantages, a well-rounded retirement strategy may involve a combination of these options to ensure financial security in later years.

Read More about NAVTTC Candidate Registration Process.

Updated Information

In a significant move to enhance retirement planning, the government has announced new incentives for voluntary pension systems. These include increased tax benefits for contributions and additional support for individuals seeking to diversify their retirement portfolios. The updated measures aim to encourage more people to invest in their future and secure a stable financial environment for retirement.

FAQs

1. Can I have more than three types of pension?

Yes, many individuals have multiple pension accounts, especially if they have changed jobs or contributed to different types of retirement plans throughout their careers.

2. How much should I contribute to my pension?

The amount you contribute to your pension depends on various factors such as your income, retirement goals, and existing financial obligations. It’s essential to strike a balance between saving enough for retirement and meeting your current financial needs.

3. What happens to my pension if I change jobs?

If you have a defined contribution pension, you can generally transfer the funds to a new employer’s retirement plan or into an individual retirement account (IRA). Defined benefit pensions may offer limited portability options, so it’s essential to understand the terms of your pension plan when changing jobs.

4. Are state pensions enough to cover all retirement expenses?

State pensions often provide a safety net, but they may not be sufficient to cover all retirement expenses, especially in regions with high living costs. It’s advisable to have additional savings or pension plans to ensure a comfortable retirement.

5. How do voluntary pension systems offer tax benefits?

Contributions to voluntary pension systems may be tax-deductible, reducing your taxable income. Additionally, the investment growth within the pension account is often tax-deferred, allowing your savings to compound over time without immediate tax implications.

6. What is the role of a Health Advisory Committee in retirement planning?

While not directly related to pensions, a Health Advisory Committee can provide insights into healthcare needs and costs, which are crucial considerations in retirement planning. It ensures that retirees have access to necessary medical services and support.

7. Can I change my investment options in a defined contribution pension plan?

Yes, most defined contribution pension plans offer flexibility in choosing investment options. You can adjust your portfolio based on your risk tolerance and financial goals.

8. How does inflation impact state pensions?

State pensions are often indexed to inflation, meaning they are adjusted periodically to reflect changes in the cost of living. This adjustment helps protect retirees from rising expenses over time.

9. What is the significance of legacy planning in pensions?

Legacy planning allows individuals to designate beneficiaries for their pension savings, ensuring that their assets are passed on to loved ones or heirs after their passing. It provides peace of mind and financial security for future generations.

10. How can I maximize my retirement savings through voluntary pension systems?

To maximize retirement savings, consider contributing regularly to your voluntary pension account, diversifying your investments, and taking advantage of tax incentives. It’s also beneficial to start saving early and review your retirement plan periodically.